In the world of personal finance, credit scores play a critical role in determining one’s ability to access loans and credit. A credit score is a numerical representation of an individual’s creditworthiness, reflecting their past borrowing behavior and financial responsibility. Lenders, such as banks, credit card companies, and mortgage providers, rely heavily on credit scores to assess the risk of lending money to potential borrowers.

What is a Credit Score?

A credit score is a numerical value that represents an individual’s creditworthiness, indicating how likely they are to repay their debts based on their past financial behavior. Lenders use credit scores to assess the risk associated with lending money to a particular individual. A higher credit score indicates a lower credit risk, making it more likely for the individual to qualify for loans and credit on favorable terms.

- Explanation of Credit Scores:

- Credit scores are generated by credit bureaus, which are agencies that collect and maintain credit information on consumers.

- The most common credit score models are FICO (Fair Isaac Corporation) Score and VantageScore, each using a different algorithm to calculate credit scores.

- FICO Scores are widely used and range from 300 to 850, with higher scores indicating better creditworthiness. VantageScores usually range from 300 to 850 as well.

- Factors That Affect Credit Scores: Several key factors influence an individual’s credit score. The weightage of each factor may vary slightly depending on the credit scoring model used. The main factors include:

- Payment History: The most crucial factor, it reflects whether the individual has made timely payments on their credit accounts.

- Credit Utilization Ratio: This represents the percentage of available credit that the individual is currently using. Lower utilization is generally better for credit scores.

- Length of Credit History: The longer the credit history, the more data available to assess the individual’s credit behavior, positively impacting the score.

- Types of Credit Used: Having a mix of credit types, such as credit cards, loans, and mortgages, can have a positive effect on credit scores.

- New Credit Applications and Inquiries: Frequent credit applications or hard inquiries within a short period may temporarily lower credit scores.

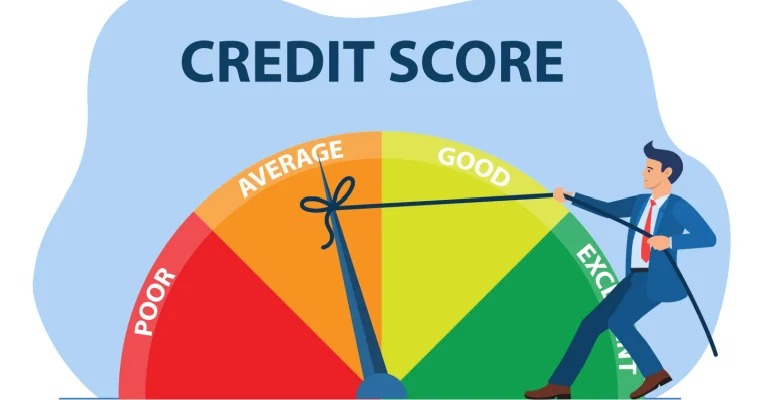

- Range of Credit Scores and Their Meanings: Credit scores are categorized into different ranges, each reflecting a specific level of creditworthiness. The general categorization includes:

- Poor: 300 – 579

- Fair: 580 – 669

- Good: 670 – 739

- Very Good: 740 – 799

- Excellent: 800 – 850

Factors Affecting Credit Scores

Credit scores are determined by complex algorithms that analyze various factors related to an individual’s credit history and financial behavior. Understanding these factors is crucial for managing and improving credit scores. Here are the key elements that influence credit scores:

Payment History:

- The payment history is the most significant factor impacting credit scores. It reflects whether the individual has consistently made on-time payments for their credit accounts, such as credit cards, loans, and mortgages.

- Late payments, delinquencies, and defaults can have a severe negative impact on credit scores, lowering them significantly.

Credit Utilization Ratio:

- The credit utilization ratio is the percentage of available credit that an individual is currently using. It is calculated by dividing the total credit card balances by the total credit limit.

- A high credit utilization ratio (using a large portion of available credit) can lower credit scores, while a lower ratio is generally considered positive for credit scores.

Length of Credit History:

- The length of credit history refers to the age of the individual’s oldest and newest credit accounts and the overall average age of all credit accounts.

- A longer credit history, demonstrating responsible credit management over time, can positively impact credit scores.

Types of Credit Used:

- Credit scoring models consider the mix of credit types an individual has, including credit cards, installment loans (e.g., car loans), retail accounts, and mortgages.

- A diverse mix of credit types can be beneficial for credit scores, indicating that the individual can manage different types of credit responsibly.

New Credit Applications and Inquiries:

- Applying for new credit can result in hard inquiries on the credit report, which occur when a lender checks an individual’s credit as part of the loan application process.

- Multiple hard inquiries within a short period can temporarily lower credit scores, as it may suggest a higher level of risk to potential lenders.

Public Records and Negative Information:

- Negative information, such as bankruptcies, tax liens, and accounts in collections, can significantly impact credit scores.

- Public records related to financial issues can stay on the credit report for several years and have a lasting adverse effect on credit scores.

How Credit Scores are Calculated

Credit scores are calculated using sophisticated algorithms developed by credit bureaus, such as Experian, Equifax, and TransUnion, or credit scoring companies like FICO and VantageScore. While the exact formulas used by these organizations are proprietary and not publicly disclosed, the general components and factors considered in credit score calculations are well-known. Here’s an overview of how credit scores are typically calculated:

Credit Data Collection:

Credit bureaus collect and maintain vast amounts of data on consumers’ credit behavior. This includes information on credit accounts, payment history, credit limits, outstanding balances, and public records (if any).

Weightage of Factors:

Each credit scoring model assigns a specific weight to the various factors that influence credit scores. The most commonly used factors include payment history, credit utilization, length of credit history, types of credit used, and new credit applications.

Payment History:

The payment history holds the most significant weight in credit score calculations. It involves analyzing whether the individual has made timely payments on their credit accounts, such as credit cards, loans, and mortgages.

Consistently paying bills on time can have a positive impact on credit scores, while late payments and delinquencies can lower scores.

Credit Utilization Ratio:

The credit utilization ratio is the next important factor. It is the ratio of the individual’s credit card balances to their total credit limit.

A lower credit utilization ratio is generally better for credit scores, as it indicates responsible credit management.

Length of Credit History:

The length of credit history also influences credit scores. A longer credit history, with well-managed credit accounts over time, can boost scores.

However, those with a shorter credit history can still have good scores if they have demonstrated responsible credit usage during that period.

Types of Credit Used:

The mix of credit types is considered to assess the individual’s ability to handle various forms of credit responsibly.

Having a diverse mix of credit, such as credit cards, loans, and mortgages, can have a positive impact on credit scores.

New Credit Applications and Inquiries:

Applying for new credit can result in hard inquiries on the credit report, which can temporarily lower credit scores.

Multiple hard inquiries within a short period may be perceived as a sign of increased credit risk, potentially impacting scores.

Conclusion

In conclusion, credit scores are fundamental components of personal finance, significantly impacting an individual’s ability to access loans and credit. These numerical representations of creditworthiness are generated by credit bureaus or credit scoring companies, taking into account various factors from the individual’s credit history and financial behavior.